Six major trends in the development of China's LED chip and packaging industry market

Published Time:

2021-08-04

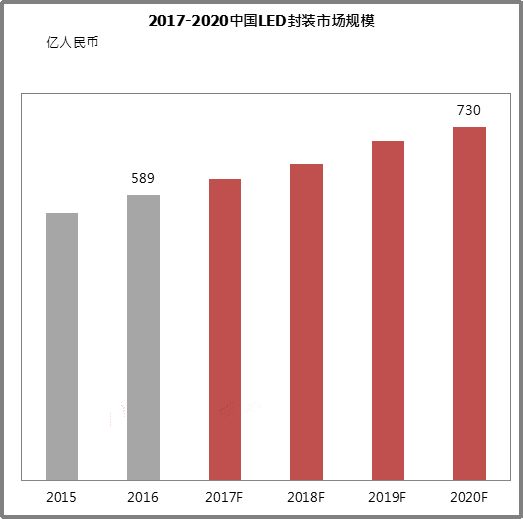

According to the latest "2017 China LED Chip and Packaging Industry Market Report" released by TrendForce's LED Research Center, the size of China's LED packaging market reached RMB 58.9 billion in 2016, representing a year-on-year growth of 6%, slightly higher than expected.

TrendForce's LED Research Center's latest "2017 China LED Chip and Packaging Industry Market Report" shows that in 2016, the size of China's LED packaging market reached 58.9 billion RMB, a year-on-year growth of 6%, slightly higher than expected. In 2016, LED prices remained stable, with some products even seeing price increases. Driven by the small-pitch display, automotive, and lighting markets, the industry continues to maintain a growth trend. Looking ahead to 2020, the size of China's LED packaging market is expected to reach 73 billion RMB.

Based on the development of China's chip and packaging industry market, the following six major trends are summarized:

。

Trend 1: Continued Rise of Chinese Manufacturers and Continuous Improvement of Domestic Production Rate

Data shows that in 2016, the domestic production rate of China's LED packaging market had risen to 67%. However, international manufacturers, led by Nichia, remain major suppliers to the Chinese packaging market. Among the top ten manufacturers, international manufacturers occupy 5 seats, with Nichia ranking first. However, the rise of Chinese manufacturers is significant, with representative manufacturers such as MLS developing rapidly. In 2016, MLS surpassed Lumileds to rank second, and NationStar Optoelectronics and Honli Zhihui further improved their rankings.

Trend 2: Stable Development of China's Lighting LED Market

In 2016, the size of China's lighting LED market reached 25.9 billion RMB, lower than market expectations. This was mainly due to the insignificant growth rate of international LED lighting demand, leading to a decline in China's total LED lighting exports. However, due to the impetus of domestic demand and price stability, the size of the lighting LED market in 2016 still maintained a 9% growth. It is expected that the size of the lighting LED market in 2017 will reach 28 billion RMB, and 36.4 billion RMB in 2020, with a compound annual growth rate of 9% from 2015 to 2020.

Trend 3: International Manufacturers Release Lighting LED OEM Orders

Due to the dominance of low- and medium-power LEDs in the LED lighting market, more and more international brand manufacturers, including Lumileds, OSRAM, CREE, Samsung, and LGInnotek, are gradually concentrating their OEM orders in China, maintaining high capacity utilization rates for major Chinese manufacturers. The top five Chinese lighting LED manufacturers are MLS, Honli Optoelectronics, Tiandian Optoelectronics, Ruifeng Optoelectronics, and Zhaozhi Energy Saving.

Trend 4: Small-Pitch Displays Drive Capacity Expansion Demand from Various Manufacturers

LEDinside analysis shows that due to the rise of small-pitch displays, display screen LEDs continue to maintain a growth trend. It is expected that the size of the display screen LED market will reach 15.8 billion RMB in 2020. In the small-pitch display LED packaging field, Everlight was the main player in the early stages, but many Chinese manufacturers have now entered this field, including NationStar Optoelectronics, MLS, and Jingtai Optoelectronics, driving capacity expansion demand from various manufacturers.

At the same time, the demand for quaternary LED capacity has also increased. According to LEDinside's analysis and statistics, San'an Optoelectronics, Wuhan Huacan, Qianzhao Optoelectronics, and Epistar all have quaternary LED capacity expansion needs in 2017.

Trend 5: The Rise of Domestically Produced MOCVD in China Will Further Reduce Costs for Chinese Manufacturers

According to data, the total number of MOCVD equipment shipments in 2016 was approximately 136 units. Veeco's equipment is mostly EPIK700, with a larger chamber. Therefore, if uniformly converted to K465i equipment, the ranking of the number of equipment units is first. Chinese MOCVD equipment manufacturers, including AMEC and Topecsh, are gradually emerging. Although their combined market share in 2016 was only 11%, after verification by clients in 2016, they will begin to enter the supply chain of Chinese LED chip manufacturers in 2017.

In the past, MOCVD equipment was controlled by European and American companies, but as domestically produced MOCVD equipment in China begins to pass verification by Chinese LED chip manufacturers, it will be introduced into some LED chip manufacturers in 2017. Due to the lower price of the equipment, it is expected to further reduce costs.

Trend 6: Rapid Expansion of Market Demand for Filament Lamps and Filament LEDs

In recent years, due to the popularity of LED filament lamps in the European, North American, and Australian markets, more and more manufacturers have entered the filament lamp field, and the market size has shown rapid growth. In 2016, the global demand for LED filament lamps was 150 million units. It is expected that LED filament lamps will continue to maintain high-speed growth in 2018, with an estimated global market demand of 600 million units. In terms of packaging product supply, the main filament LED suppliers include Yuanlei Technology, MLS, Ruifeng Optoelectronics, and Hangzhou Keguang Optoelectronics.

No. 739, Zhou Shi Road, Hezhou Community, Hangcheng Street, Baoan District, Shenzhen

Copyright © 2025 Shenzhen ETON Automation Equipment Co., Ltd. ALL Rights Reserve.